Everyone’s talking about the differences between start-ups and SMBs. Here are the secrets to underwriting both effectively.

Small businesses have historically been underserved by banks and financial service providers. Many providers simply don’t recognize the needs of small business owners as distinct from consumers or are unable to profitably service the SMB portion of the market.

It’s an undeniable fact that no two small businesses are exactly alike. They have vastly different needs, resources, and aspirations. Take, for instance, a newly formed SaaS start-up. It’s unlikely to have much in common with a 25-year-old family-run cafe, so why use one-size-fits-all approaches to serve them?

Brex is an example of a provider that is making this distinction between businesses. The organization recently announced plans to exit the SMB space, focusing on enterprise customers and start-ups instead.

But, what actually distinguishes a start-up from an SMB? According to many (including Brex), start-ups are businesses that receive some kind of ‘professional funding.’ This could be venture capital, seed funding, or funds from an accelerator. SMBs, on the other hand, do not.

Accessing capital is difficult for small businesses

Of the many and varied challenges small businesses have to contend with, accessing capital is one of the most notoriously difficult.

Our research indicates that new and small businesses are the most likely to lack access to capital, with businesses of 0-2 years being almost 3 times as likely to need external funding than businesses over two years old.

In addition, 22% of businesses with fewer than 10 employees lack access to funding vs. just 13% of businesses with 200-500 employees.

Why is accessing capital such a challenge for these small businesses? Most lenders struggle to process smaller loans for thin-file applicants profitably. Often, the cost of processing these applications and the risk they have to absorb compared to the amount the lender stands to earn simply doesn’t stack up. The end result is a large proportion of SMBs and start-ups that are unable to access the funds they need to grow.

However, with the right data to hand, underwriting these small businesses can be both straightforward and profitable. Read on to understand how.

How businesses differ

To assess the creditworthiness of businesses effectively, you need a solid understanding of how they differ, as this will determine the methods you use to evaluate risk.

For instance, start-ups typically have high growth rates and a high cash burn to match. Many aren’t even profitable until they’ve been in operation for a fair few years. This is because start-ups are usually formed to disrupt an existing process or industry, and their significant spending is often a result of investment in research and development activity. This means they’re potentially high-risk but also high-reward customers, as they tend to experience lofty growth rates as their products take hold in the wider industry.

As newly formed businesses, start-ups rarely have an established credit history, making it difficult for them to access capital via traditional routes. Instead, they may seek seed funding or capital from VCs.

SMBs, on the other hand, typically have slower growth rates and rarely raise ‘professional funding’. They do, however, tend to have lower burn rates, generate more cash flow, and could build up large cash reserves as a result of strong business performance.

In addition, they often have a much better sense of profitability and the sources of that profit. As they have typically been operating for longer, they tend to have historical evidence of performance over time.

How to underwrite start-ups

With a better understanding of the nuances of each business, you can get to work thinking about the best ways to adapt your underwriting model.

When assessing any business, you’ll want to develop an understanding of the three elements of risk: credit, fraud, and compliance. It’s important to start out by authenticating the identity of the applicant by carrying out extensive AML and KYB checks.

When underwriting start-ups in particular, it’s also crucial to understand whether or not they have received funding from elsewhere. Since they might not be turning a profit, their funding will be their main driver of growth and means of repaying your loan.

Sources of funding ?

Banking data provides the best outline of a start-up’s funding as it breaks down how much funding they’ve received, from where, and when. With banking data, you can understand:

- Any external funding they have received to date

- How much funding they have received

- Their ability to repay

- Their path to profitability

Banking data also allows you to lift the hood on a start-up’s finances and get a view into actual transactions, including information on:

- Incoming, outgoing, and overdrawn funds

- Balances held with other lenders

- Incomplete or bounced payments

- Money is directed to risky endeavors like gambling or adult entertainment

- Average invoice or bill value

- Who the SMB trades with, and how often

Revenue models ?

It’s also crucial to consider the type of start-up you are lending to. For example, many SaaS start-ups will likely charge their customers via a subscription plan (i.e. on a recurring basis). Pulling in other data sources, such as subscription data from the billing platforms, will give you a good understanding of their recurring revenue and key SaaS metrics.

Other considerations for start-ups ?

Start-ups tend to have a much higher operating spend than SMBs, so data that outlines current spending patterns and runway will come in handy. Understanding their burn rate will help you predict future changes, which indicate the ability and likelihood of repayment.

In addition, the impressive growth rate of many start-ups is something that distinguishes them from other businesses. Understanding their growth rate can help you determine whether or not the start-up is likely to survive, thrive, and ultimately repay.

How to underwrite SMBs

While the margins of a typical SMB tend to be lower than that of a start-up, they are often profitable and have a clearer sense of where their revenue is coming from. Their ability to repay will depend on cash generation rather than external funding, so you need to get a good idea of where sales are coming from and how the business is likely to perform over time. This will require more than a quick glance at their bank account.

For example, a local family-run jeweler could generate income from the following sources:

- In-store cash transactions

- Invoices

- Payments via a PoS terminal

- Payments via an online store

Accessing data from all of the platforms SMBs use allows you to get a holistic view of merchant creditworthiness and make more informed decisions.

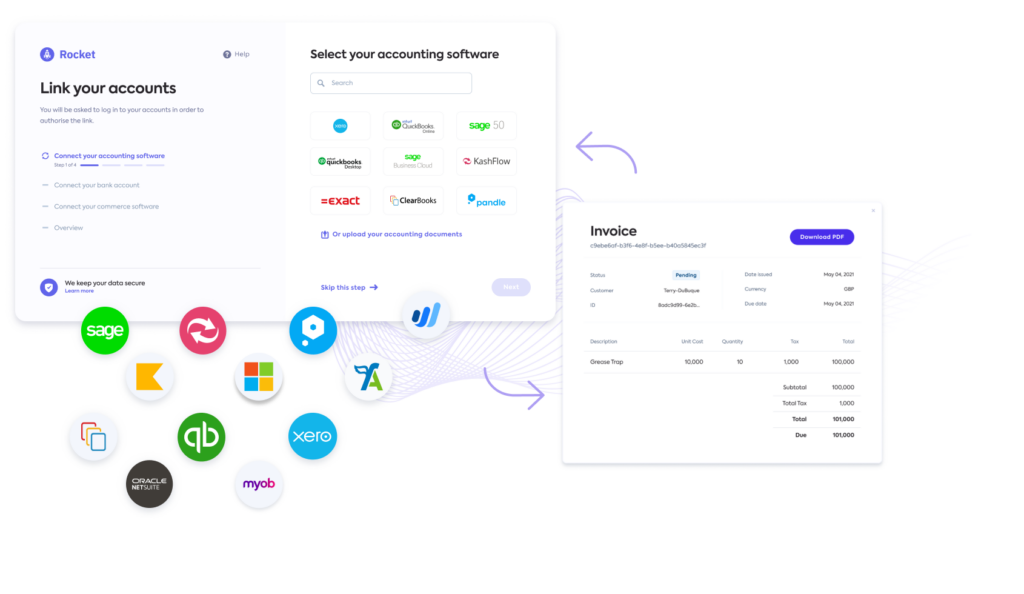

Accounting data ?

The accounting system is often the financial hub of a business, where all debits and credits are aggregated. Consulting this centralized data allows you to better understand how and when a company makes payments, identify red flags that could indicate impending bad debt, and take a proactive approach to minimize losses.

Among other attributes, accounting data can help you understand:

- Typical payment terms

- Average days to pay

- Concentration or percentage of each customer and supplier

- Paid vs. outstanding costs

- P&L statements and balance sheets

- Average invoice or bill value

- EBITDA

- Working capital

- Gross profit margin

- Collateral

- Net cash flow and surplus

Sales data ?

Unlocking sales data, SKU product information, and chargebacks can paint a clearer picture of the quality of the SMB’s products and how well they are doing. In the case of the jeweler, having a look at their Stripe, and Square account would give you a good sense of how many orders are being made both in-store and online.

Banking data ?

Banking data is an additional trustworthy and immutable data source, especially when cross-referenced with accounting data. Pulling banking data can help to lift the lid on the reality of a business’s financial health with information such as:

- Incomings

- Outgoings

- Current cash balance

- Cash flow

- Overdrafts

- Profitability

Other data types ?

To truly understand the nuances of each SMB, you may want to consider other data types. For example, for SMBs using subscription models, pulling in subscription data, from platforms such as Chargebee and Recurly, will help you break down recurring revenue, detail subscription terms, the frequency of payments, and projected income. This will give you a clearer sense of what their future revenue will look like.

For many businesses, inventory is also a key factor. Accessing inventory data from platforms like Brightpearl and Zoho Inventory can reveal overhead expenses such as the value and amount of stock a business has. You can use this information to assess future revenue by coupling it with sales data.

For larger SMBs, headcount, turnover, and payroll expenses offer insight into how well a company is functioning internally. For example, if a business has high retention rates and steadily increasing salaries, it can signal strong creditworthiness. Useful platforms include Gusto and Oyster.

How Codat can help

Our business data APIs offers accounting, banking, and commerce data in one platform, so you can access all the data you need to underwrite SMBs and start-ups, regardless of the systems they use.

We provide you with all the tools you need to continue providing capital to businesses with confidence. If you need access to real-time, relevant data to get a comprehensive view of your SMB customers, we can help. We also enrich the data through standardization and categorization techniques and provide helpful ratios and metrics to bolster your underwriting processes.

Contact us using the form below or create an account to start building for free today.